The state’s rollout of two new public safety funding mechanisms under HB 2015 continues to move ahead for city and county law enforcement agencies. AWC is running a webinar on November 19 to explain how your city can unlock new revenue through HB 2015. Here’s where the state's process now stands.

The state Criminal Justice Training Commission (CJTC) administers the $100 million public safety grants under the three-year program created by HB 2015. CJTC also verifies eligibility for cities and counties to impose the councilmanic 0.1% sales tax created as a permanent funding mechanism with the same legislation.

Grant applications for public safety projects are not yet available, though CJTC plans to post them by the end of 2025 on its dedicated HB 2015 funding program page.

For the sales tax, cities are required to verify their compliance with the new law’s policy and data requirements via the CJTC’s web site. A new update to the CJTC HB 2015 page enables cities that contract out their law enforcement services to complete a shortened application – so long as the contract agency has verified its compliance.

As cities apply for sales tax eligibility verification, CJTC has issued “conditional approvals” that allow the sales tax to be collected and detailed for each applying jurisdiction their remaining steps for full approval. After this one-time step, the sales tax becomes permanent revenue for a jurisdiction that adopts it.

Your city can learn more about how to successfully unlock this funding from CJTC officials and AWC staff at the November 19 webinar hosted by AWC. Sign up here for the webinar.

Eligibility process moving forward for HB 2015 criminal justice sales tax

October 29, 2025

The Criminal Justice Training Commission (CJTC) has received requests from 11 cities and 2 counties to verify they’re in compliance with the HB 2015 requirements for the $100 million law enforcement grant and public safety enhancement sales tax eligibility. CJTC said that in every case, the jurisdiction received a “conditional approval” and a list of next steps the jurisdiction needs to take to come into compliance within 180 days.

CJTC maintains an updated list of applicants on the agency’s HB 2015 page. As of October 29, the list includes:

- Bellingham

- Black Diamond

- Des Moines

- Edmonds

- Elma

- Kalama

- Kent

- Lynden

- Renton

- SeaTac

- Mount Vernon

- King County

- Skagit County

The state Department of Revenue reported a slightly different list of cities/counties submitted notice by October 17 that an ordinance to begin charging the new HB 2015 .1% sales tax on January 1. DOR has heard from:

- Algona

- Bellingham

- Cle Elum

- Des Moines

- Duvall

- East Wenatchee

- Edmonds

- Elma

- Issaquah

- Kalama

- Kent

- Lynden

- Renton

- Ridgefield

- SeaTac

- Seattle

- King County

There are multiple reasons a jurisdiction might appear on one list but not the other. Cities/counties had a hard October deadline to pass a sales tax ordinance and notify DOR, but HB 2015 didn’t make CJTC’s approval a prerequisite to getting DOR’s process started. Other places – Skagit County, for example – decided to start the CJTC process then start public discussion about the sales tax.

Cities that have submitted to DOR only will also need to send the verification documentation to CJTC to impose the tax.

The form to apply for the $100M grant program is still not live. CJTC says it will appear on the agency’s website “later this year.” No timeline is available.

Additionally, CJTC now provides a new form to verify sales tax eligibility for cities that contract with an external agency for law enforcement services. Contract cities can use that shorter form if the agency they contract with has separately submitted documents to verify eligibility. That new application can be found at the CJTC HB 2015 page.

AWC is hosting a webinar on how to meet the HB 2015 requirements on November 19. Please let your city officials know they can register here.

Qualify to collect the HB 2015 public safety enhancement sales tax

October 17, 2025

Cities can now move toward collecting the councilmanic 0.1% sales tax created by HB 2015 with a new Washington State Criminal Justice Training Commission (CJTC) website to send in their qualifications.

The new form is available at the “Apply Now” link from the CJTC’s information page for obtaining HB 2015 sales tax and public safety grants. It contains 17 sections and progress may not be saved. Because some of the questions require documentation that a law enforcement agency has complied with HB 2015 training requirements, cities should review the entire form and prepare all documentation for upload before working on completing the form.

Cities’ law enforcement agencies must fulfill the HB 2015 policy and training requirements in order to collect the sales tax. Cities must also enact an ordinance to authorize the tax and report that to the state Department of Revenue (DOR), which allows sales tax to begin only on January 1, April 1, or July 1, with notice of 75 or more days. The deadline for imposing the tax on January 1 has passed. Cities that pass the tax and report it to DOR by January 16 may begin to impose it on April 1.

AWC can help with this process. At AWC’s HB 2015 information website, you can learn about the details of the requirements and obtain sample ordinance language for the public safety enhancement sales tax. We are also preparing a webinar for November on how to complete the CJTC’s new detailed form and the pathways to correct any shortcomings if your city’s qualifications form is rejected.

CJTC is still working toward publishing its application for the $100 million public safety grants also created by HB 2015.

Please email us (email contacts at the top of this article) with your experience in working through the qualifications for the sales tax so that we can evaluate how this process is going for cities.

Three things you need to know to access sales tax funding allowed in HB 2015

August 15, 2025

AWC recently held a webinar covering new public safety funding pathways in HB 2015, which became law on July 27, 2025.

As we shared in the webinar, the new bill sets up two mechanisms for funding local public safety: a grant and a councilmanic sales tax. While CJTC is still working to clarify and set up the parameters of the grant, cities can now pass the councilmanic sales tax.

Cities have asked important questions about how to prove they meet the requirements of the grant, which is mandatory to implement the sales tax. There’s no need to delay this process. Section 201 (1)(d) of the bill allows a city to submit documentation to CJTC that it meets the requirements of the grant/tax “before the commission finalizes the form and manner of such submittals and may not be penalized for doing so.”

You can submit documentation of your eligibility to Gail Stone, CJTC HB 2015 Program Manager, at cjtchb2015@cjtc.wa.gov.

Read our webpage for more information about the bill along with frequently asked questions.

Three steps to passing the new councilmanic sales tax effective January 1

To move forward with passing the new councilmanic sales tax after determining your city is eligible, follow the three steps below.

- Send eligibility documentation to CJTC

You can submit documentation of your eligibility to CJTC before it completes the HB 2015 grant application process and website. Submit documentation to Gail Stone, CJTC HB 2015 Program Manager, at cjtchb2015@cjtc.wa.gov. Upon receipt, CJTC has 45 days to review the documents and notify a city of any outstanding deficiencies.

- Put the sales tax on the council agenda

Schedule the sales tax ordinance for a vote at an upcoming city council meeting. The ordinance must include a finding that the city has met the requirements of the grant (Sec. 201 (1)(a) of the bill). If you’d like to see examples to help with drafting your city’s ordinance, view these:

Please note that these examples are for informational purposes only and not intended as legal advice. Cities should work with their legal counsel for specific questions or ordinance requirements.

Once passed, the sales tax can take effect January 1, 2026, only if a city meets an October 17 deadline to notify DOR of its passed and signed ordinance. You should give your city enough time to schedule, pass, sign, and notify the Department of Revenue (DOR) before that deadline.

- Send the signed tax ordinance to DOR

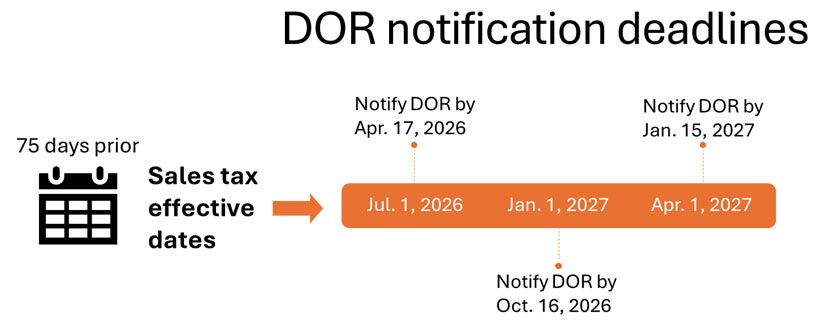

Per RCW 82.14.055, a local sales tax change may take effect no sooner than 75 calendar days after DOR receives notice of the change. Sales tax rate changes may only take effect on January 1, April 1, or July 1.

After your city passes the new sales tax ordinance, here’s how to give DOR written notification of that new tax by October 17 (to take effect January 1):

- Email Jason Hartwell, DOR Tax Administration Manager, at jasonh@dor.wa.gov; and

- Include a copy of the signed ordinance that enacts the new tax.

More information

If your city is unable to complete those steps before the October 17 DOR deadline to make the tax effective on January 1, the next available sales tax effective date is April 1 (with a DOR notification deadline of January 16). See below for the next three effective dates and notification deadlines.

The guidance on HB 2015 is evolving, and AWC is sharing information as it becomes available. Read our monthly Legislative Bulletin for the latest information and find some more helpful resources below.

Resources

Contact information